While America’s CEOs are fretting about the government’s so-called “fiscal cliff,” millions of American workers face a financial disaster that gets much less media attention. There’s a half-trillion-dollar deficit in the nation’s worker retirement benefits.

The Great Recession, which decimated retirement assets, played a big role in building this lesser-known cliff. But many corporations could have avoided the problem by shoring up these funds during the boom years. Instead, they siphoned pension assets for other profit-boosting purposes. When the pension deficits started to balloon, many corporations responded by slashing back their benefit programs.

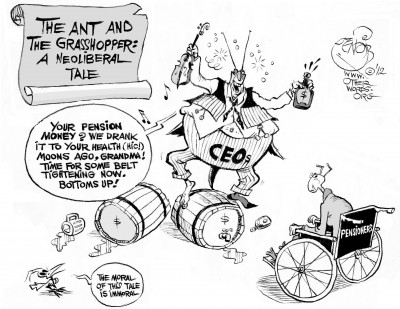

The Ant and the Grasshopper, an OtherWords cartoon by Khalil Bendib

What’s even more outrageous is that the very same CEOs who have contributed to rampant retirement insecurity are now calling for cuts to these earned-benefit programs for senior citizens.

Nearly 100 CEOs have banded together to convince the American public that Social Security and Medicare lie at the root of America’s fiscal challenges. Their “Fix the Debt” campaign features plain-spoken Americans in their ads and sounds moderate because they call for both spending cuts and revenue increases.

But the real objectives of the campaign include massive new corporate tax cuts and reduced spending on Social Security and Medicare, which would likely involve raising the retirement age.

American workers, at present, cannot collect Social Security and Medicare until age 66, the highest retirement age among rich countries. In 2020, the Social Security retirement age will rise to 67, assuring that American workers will be toiling longer than any other industrialized country for years to come. In contrast, Japanese and Chinese workers can collect their equivalent of Social Security starting at age 60.

The Fix the Debt campaign’s CEO supporters need not worry about Social Security because they’re members of the “I’ve Got Mine Club.” Fifty-four of the CEOs leading Fix the Debt directly benefit from lavish executive retirement programs. Their collective pension assets total $649 million, which comes to more than $12 million per CEO. That’s enough to garner a $65,000 retirement check each month starting at age 65 that will continue for as long as they live, according to a new report by the Institute for Policy Studies, which I co-authored. In contrast, the average retiree receives just $1,237 from Social Security each month.

Yet, the firms headed by Fix the Debt CEOs owe their U.S. pension funds more than $100 billion, according to the IPS study. U.S. law requires corporations to keep their pension debts to manageable levels, but this pressure has often resulted in benefit cuts.

General Electric, which has a staggering $22 billion pension deficit, shut down its pension fund last year, saying it had become a “drag on earnings” (at a whopping cost of 13 cents per share, according to their estimates). Like many other firms, GE has shifted new employees to a less costly 401(k) plan, putting the risk for poor stock market performance onto employees.

Beware of wealthy CEOs who are lecturing the rest of us about tightening our belts. American workers would be far better off if CEOs worried more about fixing their own companies’ pension debts.